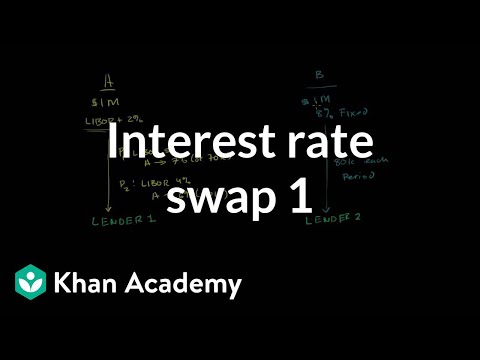

Let's say that we've got Company A over here and it takes out a $1 million loan. It plays a variable interest rate on that loan, paying LIBOR plus 2 percent. LIBOR stands for London Interbank Offer Rate and is a major benchmark for variable interest rates. Company A pays this interest rate to the lender who loaned them the money. Every period, the amount paid by Company A depends on the LIBOR rate. For example, in period 1, if LIBOR is at 5%, Company A pays 7% or $70,000 to the lender. In period 2, if LIBOR decreases to 4%, Company A pays 6% or $60,000 in interest. Now let's consider another company, Company B. It also borrows $1 million but at a fixed rate of 8%. Regardless of what happens to LIBOR or any other benchmark, Company B will always pay 8% of $1 million in each period, which amounts to $80,000. Unfortunately, neither of these parties is satisfied with their current situations. Company A dislikes the variability and unpredictability of LIBOR, making it difficult for them to plan their payments. On the other hand, Company B feels that they are overpaying for interest compared to Company A. To address their concerns, they can agree to swap some or all of their interest rate payments through an arrangement called an interest rate swap. For example, Company A could agree to pay Company B 7% on a notional $1 million loan amount. No actual money changes hands in this swap. In doing so, Company A can mitigate the variability of LIBOR and have a more predictable payment amount. Company B, on the other hand, can benefit from a lower interest rate and potentially take advantage if LIBOR goes down.

Award-winning PDF software

Section 6621 interest rate 2024-2025 Form: What You Should Know

Percentage points; and (b) the amount of the deduction allocated to the taxpayer under section 6646, in computing any other income and deduction, must be decreased, on a dollar for dollar basis, by 12.5 percentage points. Subsection 6642(i) — Computation of Interest is calculated by a daily interest method which consists of two parts. The first is the basis for the subject item and the second is the daily return on account of interest. The basis under this method is the amount of the subject item. Thus, to calculate interest, the subject item must be sold to the taxpayer or to an unrelated person. If the subject item is a property that is not a section 6662 asset as defined in §1.662-2(d)(2), interest on the subject item is calculated by the percentage increase or decline in the interest rate on the same type of security sold or used to pay interest on a prior year's tax year return. 26 USC 6621: Determination of rate of interest — U.S. Code. For purposes of computing the interest rate on any overpayment under section 6641 for periods after the applicable date, the rate of interest shall be reduced by 12.5 percentage points; and subsection 6641(i) — Computation of interest — For purposes of computing the interest rate on any underpayment under section 6652 for periods after the applicable date, the rate of interest shall be reduced by 12.5 percentage points. Subsection 6652(n) — Computation of Interest is computed by a daily interest method which consists of two parts. The first is the basis for the subject item and the second is the daily return on account of interest. The basis under this method is the amount of the subject item. Thus, to calculate interest, the subject item must be sold to the taxpayer or to an unrelated person. If the subject item is a property that is not a section 6662 asset as defined in §1.662-2(d)(2), interest on the subject item is calculated by the percentage increase or decline in the interest rate on the same type of security sold or used to pay interest on a prior year's tax year return. 26 USC 6621: Determination of rate of interest — U.S. Code.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 2220, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 2220 Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 2220 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 2220 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Section 6621 interest rate 2024-2025